By Rockefeller Philanthropy Advisors | January 24, 2022

The COVID-19 pandemic has put many small and medium enterprises at severe risk of running out of money. This is due to decreasing income especially during the heat of the pandemic occasioned by the economic shutdown. Clearly, the purchasing power of most consumers was reduced even as businesses either scaled down operations or completely shut down. In Nigeria in particular, small business owners and managers have continued to lament the decline in income needed to run and sustain their business operations. A critical implication of this is that these small businesses apart from meeting other economic and social obligations are also unable to save money.

Researchers have established a positive relationship between savings and income. Also, savings and investments have been linked together. Economists opine that savings and investments are the preconditions for growth and development of many economies. Data from early survey by Government Enterprise and Empowerment Program (GEEP) showed that over 90% of small businesses had their savings depleted during the Covid-19 crisis. According to the survey, most of the SMEs save less than before the pandemic. However, the obvious decline in the purchasing power of consumers especially at the peak of the pandemic and the partial lockdown and later full lockdown worsened economic activities thereby impacting heavily on the income of especially small businesses.

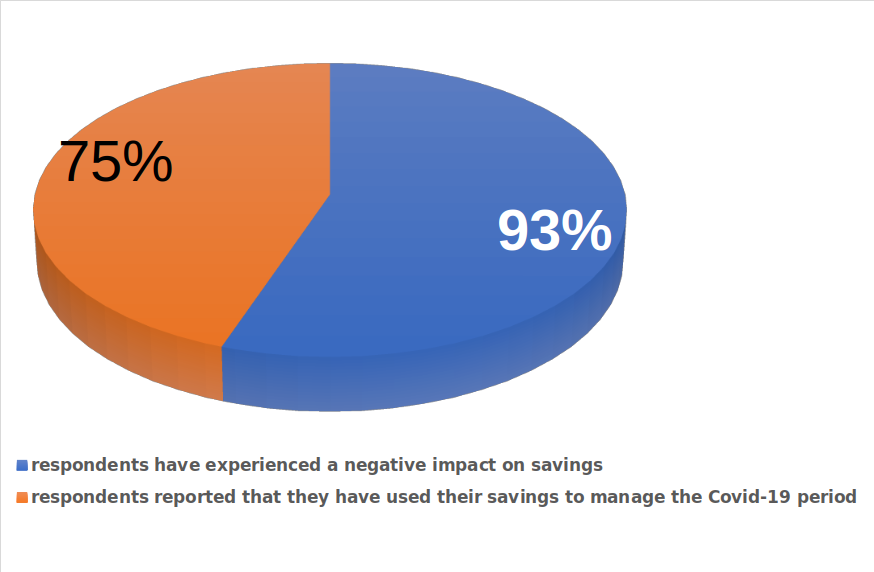

Although, there were early signs of improvement especially after the re-opening of economic activities, small businesses are still struggling to make enough savings needed to take care of business exigencies. This was reflected in the GEEP survey data which indicated that 48% of the sampled small businesses were able to save more few months after the lifting of the lockdown. However, with changes in macroeconomic indicators including inflation rate, exchange rate etc. the savings culture of small businesses may not have witnessed significant improvements. Savings have been described as important strategy for businesses and a key coping mechanism used by small businesses for their operations. The use of savings has proven to be a critical resource in times of crisis. In essence, apart from crisis period, savings enable small business owners and managers to take care of urgent needs and make investments. Insights from the GEEP survey show that nearly 75% of the respondents reported that they have used their savings to manage the Covid-19 period. Given that 93% of the respondents have experienced a negative impact on savings since the beginning of the pandemic, this data indicates some relief in this area.

Savings have been described as important strategy for businesses and a key coping mechanism used by small businesses for their operations. The use of savings has proven to be a critical resource in times of crisis. In essence, apart from crisis period, savings enable small business owners and managers to take care of urgent needs and make investments. Insights from the GEEP survey show that nearly 75% of the respondents reported that they have used their savings to manage the Covid-19 period. Given that 93% of the respondents have experienced a negative impact on savings since the beginning of the pandemic, this data indicates some relief in this area.

Globally, smaller businesses face unique and specific problems around access to external capital. These issues are often compounded by their nature and a lack of tangible and physical assets which are used as collateral against loans. The implication is that many of the small businesses are unable to meet the requirements for formal funds. In essence, many small businesses have an over-reliance on internally generated funds to capitalize their operations and provide the necessary liquidity to fund their day-to-day operations.

Globally, smaller businesses face unique and specific problems around access to external capital. These issues are often compounded by their nature and a lack of tangible and physical assets which are used as collateral against loans. The implication is that many of the small businesses are unable to meet the requirements for formal funds. In essence, many small businesses have an over-reliance on internally generated funds to capitalize their operations and provide the necessary liquidity to fund their day-to-day operations.

In improving the culture of savings, SME leaders need to be deliberate in recognizing savings as a strong culture in business growth and survival. There is the need for more savings by small business owners and managers to support business operations. This could help reduce unemployment and later translate to a better gross domestic product (GDP) and economic development.

Small businesses can improve their savings by cutting down on their operational costs especially unnecessary expenses. Small business owners and managers can also negotiate more with vendors on possible reduction of costs. This is because vendors also want to be in business. SMEs can save more if they earn more. In essence, there is the need for SMEs to increase their ability to earn more. Embracing digital marketing and online sales could boost the earning capacity and thereby increase the saving power.

Cooperative or microfinance groups have proven to be an important means of savings especially for small businesses. SME leaders should be encouraged in joining microfinance groups or cooperative societies or other associations that organizes periodical monetary contributions. There is also the need for SMEs who belong to such microfinance groups or cooperative societies to know that the essence of joining such groups is to grow their businesses and not to acquire household items. Government and SME-allied institutions need to reorientate small business owners and managers on the real motive of savings.